PwC opened up a discussion on the future of audit through a series of roundtable events across the country, surveys of the UK’s business and investment communities, and an open invitation to participate online. This captured the views of a wide range of organisations and hundreds of individuals.

The stakeholders’ requirements were recorded in PwC’s subsequent Future of audit report and are shown below in bold font. Following each set of requirements is a bulleted paragraph explaining how the requirements are met by the Perendie platform ®.

A greater focus on the future, Clearer signalling of risk, A stronger going concern assessment, A stronger viability statement

- The platform uses causality to predict the probability of outcomes being delivered.

Greater transparency through the auditor’s report

- The platform displays a single picture of everything the organisation is aiming and likely to achieve, do and employ.

Simpler, more accessible corporate information

- The information is visible to everyone allowed to access the platform.

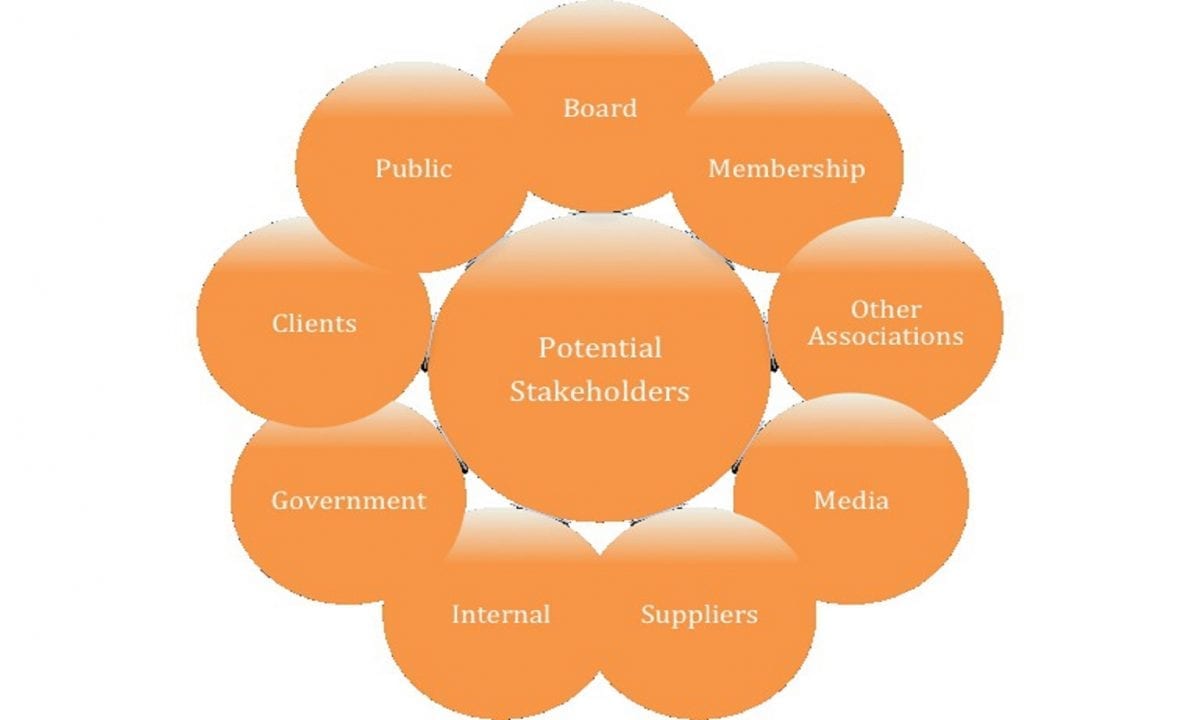

Seeking a better understanding of the needs of a wider stakeholder community

- Anyone allowed to access the platform can offer to contribute to the delivery of any outcome.

A divergence in views about auditing non-financial information

- Financial and non-financial information are integrated on the platform, and located with the outcomes they inform.

An appetite for financial information reported outside the financial statements to be included in the audit

- All relevant information and only relevant information is included on the platform.

A desire for the information that is audited to be customisable

- The organisation decides what to include on the platform.

Recognise the needs of smaller businesses, Look at whether to audit smaller privately-owned companies at all, Bring greater scrutiny for companies with the greatest societal footprints

- The platform is infinitely adaptable to the needs of the organisation and its environment, and is applicable to any sort of organisation.

Optimism about the potential impact of technology, Caution about the limits of technology, A belief in the continuing value of human judgement

- The platform facilitates human judgement by providing all the information required and only the information necessary to make informed judgements.

Differences in opinion about whether today’s audit is ‘broken’

- The platform contains a causal business model which predicts whether outcomes will delivered, and so provides greater assurance than is provided by retrospective audit and subjective judgements.

Questions about how to define quality, A desire for a culture of challenge in audit teams, Demands for the audit to better communicate the risks of fraud

- The integration, transparency and predictability provided by the platform enable anyone with access to “audit” the company at any time and challenge management about issues they notice, automatically improving the quality of audit.

A request to increase the responsibilities of company directors

- The benefits listed above depend on companies using the platform; hopefully the assured increase in productivity and profitability arising from its use would encourage its adoption.