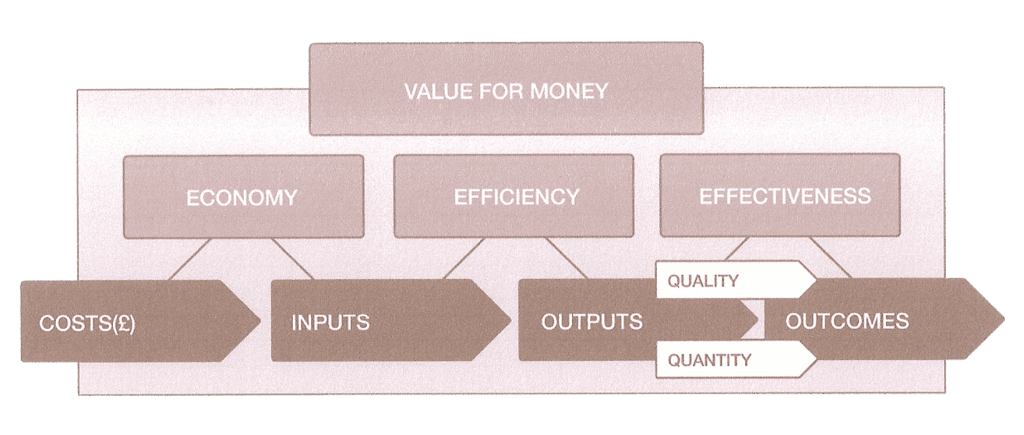

The cost structure of an organisation is defined as the distribution of costs among the processes an organisation uses to deliver its products or services. An outcome is defined as the result and benefit of achieving an objective, or a desired future state.

Of the 670 organisations we have researched, few ever rethink their cost structures, though all frequently look for cost reductions. The relationship between money and outcomes is largely unknown, and there is no way of ensuring that money is converted into the desired outcomes. They believe that more money will produce better outcomes – but it won’t because they don’t have a system to turn money into outcomes. They think that reorganisation will reduce cost – but reorganisation de-motivates people, and doesn’t change what they do or how they do it.

So what is to be gained from rethinking cost structures, and what is lost by restricting attention to cost reduction?

Drawbacks to current cost reduction strategies

The conventional approach to cost management is to start with the costs and find ways to prevent or reduce them. Well of course, what else could you do? Seems obvious, doesn’t it?

Current cost reduction strategies include outsourcing, category management, process standardisation, leverage of purchasing power, low cost market procurement and some Internet sales models. These strategies work and are very successful in reducing costs.

However, they have defects in common:

- They don’t help you to rethink your cost structure – they reduce costs within the existing structure.

- They don’t tell you which cost reduction strategy should be applied to which area of the business and when.

- They don’t tell you why you’re spending what you’re spending on what.

- They threaten product / service quality.

- They don’t deliver value for money and the outcomes you need to deliver.

- They potentially deprive strategy of the resources required for implementation.

- They don’t make optimum use of resources.

Looking at cost from a different perspective

Here’s a different way to look at it. Instead of letting your cost structure determine your outcomes, let your outcomes determine your cost structure. Instead of starting with cost reduction strategies, start with an outcome delivery strategy. Such an approach lets you have your cake and eat it. You get all the benefits of conventional cost reduction strategies but you also:

- Rethink your cost structure.

- Find out which cost reduction strategy should be applied to which area of the business and when.

- Discover why you’re spending what you’re spending on what.

- Increase product / service quality.

- Deliver value for money and the outcomes you need to deliver.

- Align resources with the strategy.

- Make optimum use of resources.

Consider an analogy

The Titanic had a double-bottomed hull that was divided into 16 watertight compartments. Because four of these could be flooded without endangering the liner’s buoyancy, it was assumed unsinkable. Shortly before midnight on 14th April 1912, the ship collided with an iceberg; five of its watertight compartments were ruptured, causing the ship to sink at 2:20 AM on 15th April.

What lessons can be applied from the Titanic to rethinking cost structures?

Firstly, take a unified approach. Instead of relying on watertight compartments, treat the organisation as a whole. Instead of operating like a ship, whose purpose is to resist its environment, operate like a fish which lives in and co-operates with its environment.

Secondly, look ahead. The pace of change continually increases and so does the need to rethink cost structures. Thinking ahead to what the future outcomes will and should be gives you the ability to define the required cost structure.

Thirdly, use your picture of the future to challenge assumptions and convention. Starting with outcomes gives you a cost structure from which to challenge existing practices, procedures, processes, programmes and even products.